![]() By Staff

By Staff

January 8th, 2018

BURLINGTON, ON

Canada’s major cities tend to understate revenue and spending, wait too long to release budgets, and confuse taxpayers with obscure figures in their financial reports, finds a new study from the C.D. Howe Institute.

The C.D. Howe Institute is an independent not-for-profit research institute whose mission is to raise living standards by fostering economically sound public policies. Widely considered to be Canada’s most influential think tank, the Institute is a trusted source of essential policy intelligence, distinguished by research that is nonpartisan, evidence-based and subject to definitive expert review.

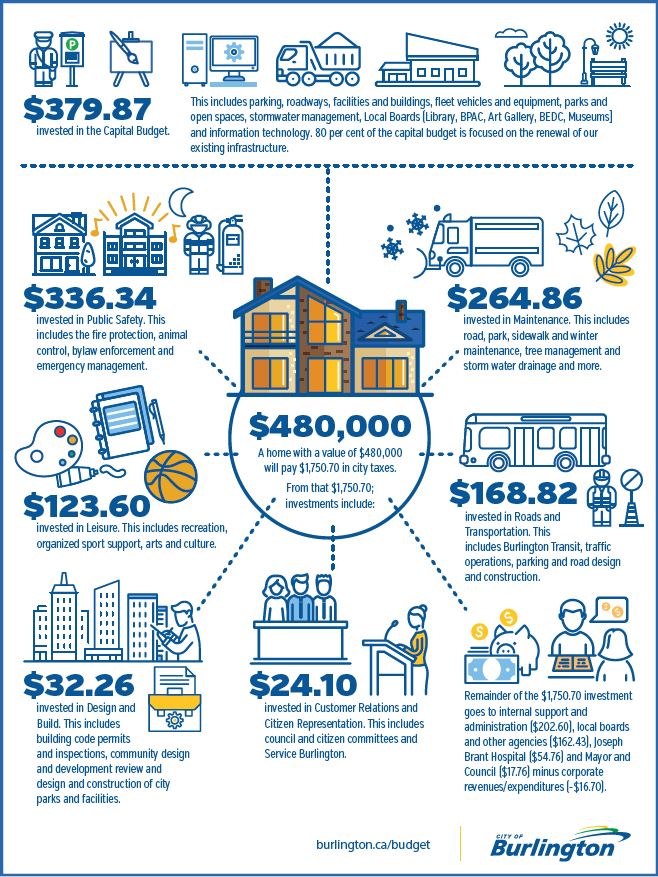

The Infograph does let you know where your dollars are going – is that enough? For 2017, each $100,000 of an urban residential assessment amounts to approximately $365 in property taxes for city services.

In the 2017 edition of the Institute’s annual municipal fiscal accountability report card, titled “Fuzzy Finances: Grading the Financial Reports of Canada’s Municipalities,” the authors “found a dramatic divergence in the quality of financial reporting among municipalities”. “Sadly, this year’s report card highlights some marked declines in municipal fiscal accountability.”

While Burlington wasn’t one of the municipalities that was reported on the questions the authors of the report raised are still very relevant; especially for a city that has raised the tax rate by close to, sometimes above 4% each year for at least the past three years.

Joan Ford, the city’s Director of Finance knows where every dollar comes from and where every dollar gets spent.

The staff within the Finance department know their stuff; they have their fingers on every piece of information and when they are asked a question they have a direct answer – no “flim flam” from that department.

Where they err is on making the information available to the public and reconciling what they promise and what they deliver. Basically – the accountants aren’t as accountable as they need to be. The department has the capacity to better inform the public.

They aren’t told to do so by the City Manager who calls all the shots and they aren’t directed to do so by the elected city council.

City manager James Ridge.

There was a memorable occasion during the discussion of last year’s budget when James Ridge, the city manager, said that staffing needs just “bubble up” during Leadership Team budget discussions. At the time Ridge was asking for a $500,000 addition to the base budget. Councillor Meed Ward tried to get that pared back to $300,000 for the first year – she didn’t get the support she needed.

Jack Dennison, probably the best financial mind on council wasn’t aware that the $500,000 was being put into the base budget.

Much of that spending Ridge was asking for was to be on the Grow Bold initiative – and we know what we got for our money on that one.

Burlington has always had a small group of citizens who get out to public meetings to review budgets, policy proposals and share ideas. In that regard we are fortunate. Unfortunately – the city no longer holds this kind of meeting – they did do a telephone call in program instead.

The C D Howe Institute “urges municipalities to adopt accrual accounting in budgets – municipal governments should present their annual budgets on the same accounting basis as their year-end financial statements.

Present headline figures early and prominently in budgets and financial reports –municipalities need to display the key numbers in a more accessible manner. Burlington puts up some detailed Infographics that go part of the way.

Show gross, consolidated, municipality-wide spending – municipal budgets should show gross spending and revenue so that users of financial statements have a comprehensive overview of a government’s fiscal footprint.

Explain deviations from budget plans – municipalities should prominently display tables reconciling year-end results with budget promises.

Publish budgets and financial reports in a timely manner – municipalities should approve expenditures before the government spending happens.

Burlington misses this mark by a wide margin.

Municipalities are not allowed to operate at a loss. When Burlington’s Finance department reports on how they managed the collection and spending of taxes they have gotten into the habit of using the phrase a “positive or a negative variance” – they don’t like saying there was a surplus.

There is always a surplus – sometime a huge amount – it was once as high as $9 million. That surplus gets distributed into the numerous reserve funds the city has to draw on – that’s what prevent any kind of a loss in any one year. When the reserve funds are close to being depleted the city will include a top up amount in the next budget.

The favourite reserve fund is the Tax Stabilization account – it is a sort of the piggy bank that council can always go to when funds for something unexpected is needed.

“Clearer, more consistent figures and better accountability for hitting or missing budget targets would bring the financial management of municipalities better into line with their fiscal impact and their importance in Canadians’ lives,” the authors conclude.

In a CBC radio interview earlier this morning the authors of the report touched on citizen participation in the creation of the budget. A couple of public budget session ago Vanessa Warren, an advocate for more significant public involvement in the creation of the budget, asked why the meeting was being shown a budget but not being asked to be involved in the creation of that budget.

Burlington does a survey asking what people think of the budget – and always gets high marks. Councillor Dennison has not been known to question the validity of that survey.

City council passed a bylaw allowing the Finance department to send out interim tax bills for a budget that has yet to be approved.

Unfortunately, Burlington’s budget process leaves much to be desired. First of all, there is no true budgeting. Proper budgeting requires zero-based budgeting where a line-by-line examination of all expenditure categories is evaluated; I suspect that a significant part of the budgetary problem in Burlington is that each department submits last year’s figures and adds on. Secondly, the mayor and council have strayed dramatically from sound management of essential services in Burlington and spent too much money on “frills and nice to haves”. Third, the mayor and council like to hide their profligacy behind the financial discipline of the region–you’ll never hear Goldring talking about the increase in City taxes–it’s always “the overall tax increase”. Lastly, how long does the mayor and council believe that residents can support tax increases twice the rate of inflation–many seniors are on fixed incomes and when taxes rise, their standard of living falls.

All great points Phillip!

What I would like to know see is a comparative analysis of how the City of Burlington’s financial situation, organizational structure and key performance indicators compare with other municipalities across Ontario. Some measures to consider include:

1) our annual employee turnover rate;

2) the average number of sick days per employee;

3) the number of employees on STD and LTD, as well as the $ cost;

4) the growth in overall complement subdivided by department;

5) the percentage of employees on the Public Sector Salary Disclosure Act in relation to the total number of employees;

6) the $ amount that was spent last year on consultants and third party service providers, and for what;

7) the $ amount that was spent last year on executive search firm retainers;

8) the % increase in the size of the benefits budget year over year.

I would love to know how the City justifies a 4% increase when most employees, seniors and persons on fixed income will be lucky to see a 1% gain.